This last quarter has been rough, and this last month especially so. Throughout the first week of May, stocks went on a rollercoaster that included skyrocketing gains on Wednesday the 4th… only to be followed by a crushing 5% loss the following day.

In a word, it’s been scary. Q1 2022 saw over $380 billion wiped out between Apple, Microsoft, Google, and Amazon alone. Since those four names are key holdings in nearly all pension funds, sovereign funds, retirement accounts, and even many, many trading accounts, that loss has been felt everywhere.

So everyone wants to know:

- What the bleep is going on?

- How much worse is it going to get?

- What can I do to protect my investments?

Per usual, I won’t claim to have decisive answers to all of these questions. But there are some pretty clear answers to the first one, and we can at least make educated guesses about the second. As for the third, we’ll review some key components of a good investing game plan. Because times like this are exactly the reason why you should have such a game plan.

What the $%#@! is going on??

Last call at the bar

Despite all the political and economic turmoil happening everywhere, 2021 was an almost freakishly good year for the stock market overall. First, it enjoyed remarkable stability, with a range of only 5.2% between its highest and lowest points. But it was extremely prosperous as well, with the S&P 500 hitting new all-time highs a record-breaking 70 times.

Paradoxically, we have the pandemic to thank for this. Or, at any rate, the pandemic response: the combination of massive cash outflows and rock-bottom interest rates turned the stock market into something of a party for investors across the board. New retail traders flooded in, SPACs took off, and consumers went on a spending spree.

But. Everyone knew the party would end when Dad got home; that is, once the Fed started raising rates again. So in addition to the general exuberance, there was also a sense of trying to squeeze out every last drop of profit while the getting was still good. My guess is that this weird emotional cocktail intensified as the expiration date drew closer, leading to the whiplash highs and lows of early 2022.

Which brings us to May 4, when the Fed announced a rate increase of 0.5%… and the Nasdaq shot up 3% by the end of the day. This reaction would make zero sense if it weren’t for the other part of the Fed’s announcement: that rates would not increase by 0.75%. Although that probably doesn’t sound like much of a concession, it seems traders were downright jubilant about it.

It’s not unlike a child who gets disproportionately excited when his parents say he can play for five more minutes before going to bed. To a kid, five more minutes sounds like forever… but he’s in for a rude surprise when he finds out how short it really is. Which brings us to May 5.

A painful reality check

Despite stocks’ rockstar performance – and the Fed’s relative clemency – several inconvenient truths remained stubbornly in place. I suspect the recollection of those truths caused some investors to sober up quickly. Once they did, more and more rapidly followed suit, and the would-be sobriety spiraled into something like panic.

What are some of these inconvenient truths? Well, a lot of things; but chief among them was (still is, really) a triple-whammy of increased costs for firms:

- Skyrocketing wages due to an apparent labor shortage

- Skyrocketing material costs due to ongoing supply chain snarls

- Imminent interest rate increases, which especially impact companies – like tech-based Nasdaq leaders – that rely heavily on debt financing.

Although these are significant pressures, they’re not immediately visible the way big headlines – like a Fed announcement – are. So investors may not respond to them quickly or dramatically; but they will respond eventually. And in this case, just a few doing so may have set off a chain reaction.

The sell-off snowball effect

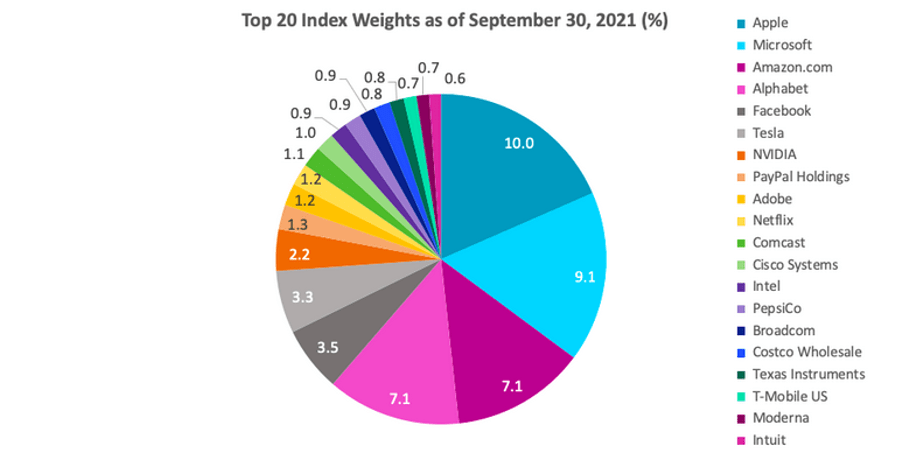

Nowadays, a significant number of daily trades happen through mutual funds and ETFs rather than individual company stocks. So when investors in such funds want to “risk off,” they’re not necessarily choosing to sell Apple or Amazon or Microsoft in particular. Rather, they end up selling a bunch of stocks indiscriminately.

For example, if you invest in an index fund based on the NASDAQ Composite, that means you’re investing in the following:

So if and when you sell off your shares of that index, you’re actually selling pieces of 3,000 different companies. But notice that, in this case, you’re selling far moredollars of Apple, Microsoft, Amazon and Alphabet stock than anything else. Now multiply this dynamic across millions of investors, trading in thousands of similarly weighted funds…

Turns out it doesn’t take a whole lot for those mega-cap stocks to whipsaw all over the place. And when they do, they drag all kinds of other equities around with them, sending huge ripples across the entire market. Add this dynamic to the perfect storm of other stuff going on – rate increases, record inflation, and you have yourself a mess.

Learning something new?

Keep learning with our weekly money and market insights!

How much worse will it get?

I have no idea, really. We are not yet halfway through the year – and, as with the 2014 Seattle Seahawks, the market’s second half often looks different than the first. For better or worse.

It’s pretty hard to say that any economic event is objectively good or bad for everyone. With that in mind, there are a few potential pros and cons to the current environment that are worth mentioning:

Short-term bear, long-term bull?

As analyst Ben Carlson notes on his blog, this year is currently on track to be among the 10 worst in stock market history. As of this writing, the YTD return on the S&P 500 is -13.38% – earning 2022 a place in that rogues’ gallery.

Again, things could change a lot over the next five months, so who knows if 2022 is going to keep that unenviable distinction. Even if it does, however, Carlson goes on to make a critical point: the lower stocks go the higher your expected returns are going out into the future.

Note the two columns on the right of the above table: within five years of each of those doozies, the market made substantial (sometimes huge) positive returns. So depending on your time horizon, this could actually work out in your favor in the long run.

Buy low so you can sell high?

Does the above mean I am actually bullish on stocks right now? Well, no. I do not get bullish simply because prices go down – I get bullish when stocks become undervalued. The difference is critical.

So far this year the NASDAQ is down 23% and the S&P is down 13%. Have the markets overshot the downside? Is it time to buy? Is this my big opportunity???

For certain stocks yes and for others no. If we looked at all the companies in our investable universe and averaged them together, it appears that, no, we are not yet in bargain territory. Based on the prices of (most) stocks, the expected free cash flow of their companies, and the macroeconomic environment, it appears that a lot of stocks today are reasonably priced but have not overshot their downside.

What if I don’t have time??

Many seem to think the sky is falling, but I just checked – it’s definitely still there. Still, I know some of my readers are starting to feel panic. Not just for what has happened, but also for what might come next.

And you know what, I understand. It is okay to feel panicked. Just be very careful not to act panicked.

“But Graham, I am [retired/conservative/impatient]; I do not have time to wait for the market to come back if it falls much further!”

If you are retired, keep in mind that you are NOT exposed to the same risks as “the market” at large. What you see on the charts of major indices isn’t the same as what appears in your portfolio – while you have certainly taken a hit, it is not to the tune of 30%, 20% or likely even 15%.

Times like this are exactly the reason why you have a gameplan. So, as an example, let’s look at a few key elements of the one my clients use.

What can I do about it?

While the following principles probably can’t reverse whatever damage you’ve already endured – nor guarantee safety from future losses – they’re invaluable pointers on how to keep your head when everyone else is losing theirs. That often makes all the difference in the long run.

1. Don’t buy/sell stocks based on price

Sound counterintuitive? Actually it’s not.

Consider: when everyone is busy trying to predict the behavior of stock prices, they often ignore those stocks’ underlying value: corporate earnings. And those two figures are by no means in lockstep, as the below chart demonstrates.

This offers a stupidly simple method to investors who are willing to actually research the fundamentals:

- Buy assets when they’re undervalued

- Trim assets when they’re overvalued

But how do you know which is which? I’m glad you asked…

2. Don’t trade stocks – invest in companies

As the famous (and hugely successful) investor Peter Lynch put it, “I’d love to get next year’s Wall Street Journal; that’d be very helpful. But I don’t know what’s going to happen in the future; I want to find right now.”

And we very much agree. That is, we don’t buy a company’s stock for what it will do in the future; instead, we focus on what it’s actually doing in the present time. What a concept!

Successful investing has far less to do with monitoring share prices, and far more to do with the underlying health of a company – both short- and long-term. In this year’s first quarter, for example, 62% of companies in the S&P saw a drop in stock price. However, only 40% of companies actually experienced a decline in their profits.

Hmmm! Can you say, “value opportunity?”

3. Don’t try to time the market

Seriously, don’t.

Our firm did a lot of selling in the last quarter of 2021; a move that, obviously, worked out in our favor. This wasn’t just good luck, but it wasn’t an attempt to time the market either. We just knew that (a) stock prices were high, and (b) the low interest rate party would end soon, as per the Fed’s announcement.

It’s not like we had some exceptional insight here. Everyone knew prices were high. Everyone knew the Fed planned to start raising rates. But greedy market timers clung to their high-flyers in hopes of squeezing the last few drops of market gains. Then they got burned once the big sell-off actually happened because (surprise surprise) it’s hard to get ahead of a market-wide landslide.

Fortunately, 0% of my investors will need to liquidate stocks to cover a short term (2 years or less) expense. This is because they’re not investing short-term cash in long-term investment vehicles. Stocks are for the long-term; and if you invest accordingly, you’ll be far less tempted to gamble with them.

The Game Plan’s Weakness

In short: it’s hard. Which brings me to the best advice I’ve ever received from another financial advisor:

“If your clients are comfortable all the time, then you are not doing your job.”

There are ways to get and/or stay wealthy; and then there are ways to avoid market fluctuations.

Unfortunately, you can’t have both – but there are ways to get wealthy while managing market fluctuations. And that is what the game plan is for.