Big news this week as the Fed has decided not to raise interest rates again (gasp!). For this month, anyway; they may or may not decide to resume course in July. But either way, this is an exciting development as it means inflation is slowing down. Or at any rate the Fed thinks it is.

It is also a little odd, however, in light of the fact that Americans’ collective credit card debt is about to hit the $1 trillion mark.

Back in November we discussed how consumers can perpetuate inflation if they continue to pay for overpriced stuff – by putting that stuff on their credit cards, for example. Conversely, increased credit card spending may indicate that things are still too expensive for consumers to pay for them with real money.

So does this mean the Fed is out to lunch and inflation is sticking around after all? Not necessarily.

Credit card debt is no joke, of course. But the mere fact that its raw dollar value is increasing does not mean much by itself. Remember, the raw dollar value of most things increases over time – so the real question is how much CC debt has increased compared to other things.

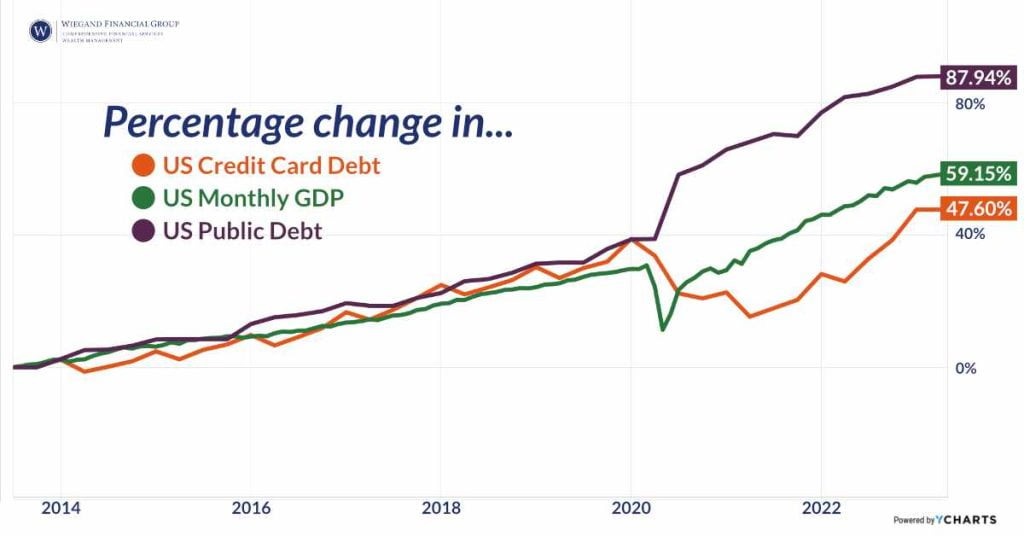

Both GDP and personal income, for example, have grown more in the past decade than CC debt has. While this does not prove anything outright, it does suggest that Americans’ overall credit card spending has not outstripped their productivity. Broadly speaking, anyway.

As scary as $1 trillion of credit card debt sounds, it is not really news in the big picture. Now for an additional piece of perspective, throw national debt into the mix:

While CC debt is more or less back to its pre-pandemic trajectory, public debt (government debt) shows little sign of slowing down. That may be a bigger cause for concern – but you already know that. And, sadly, there is little you or I can do about it. It is always better to focus on what we can control, which brings us back to a familiar conclusion: Regardless of whether or not “consumers” as a whole are putting too much on their credit cards, it is never a bad time to practice discipline in your own spending.