Even if you have never heard of it before, the term “infinite banking” is probably enough by itself to set off alarms in your head. And it doesn’t help that, if you have encountered the concept before, it was likely through a slick-haired social media influencer like this one:

Hopefully you know to take this type of quick video pitch with a big grain of salt. Still… it does sound appealing. You get to pull money out of your life insurance policy, and yet the money somehow remains in the policy at the same time? And it keeps earning you interest? Sounds like a good deal!

So good, in fact, that you might assume it is a scam.

That was my assumption too, and I was hoping my research for this post would turn up some slam-dunk proof. But the reality is more complicated. I can tell you that infinite banking is not actually a scam… but it is hardly a miracle pill either.

How does infinite banking work?

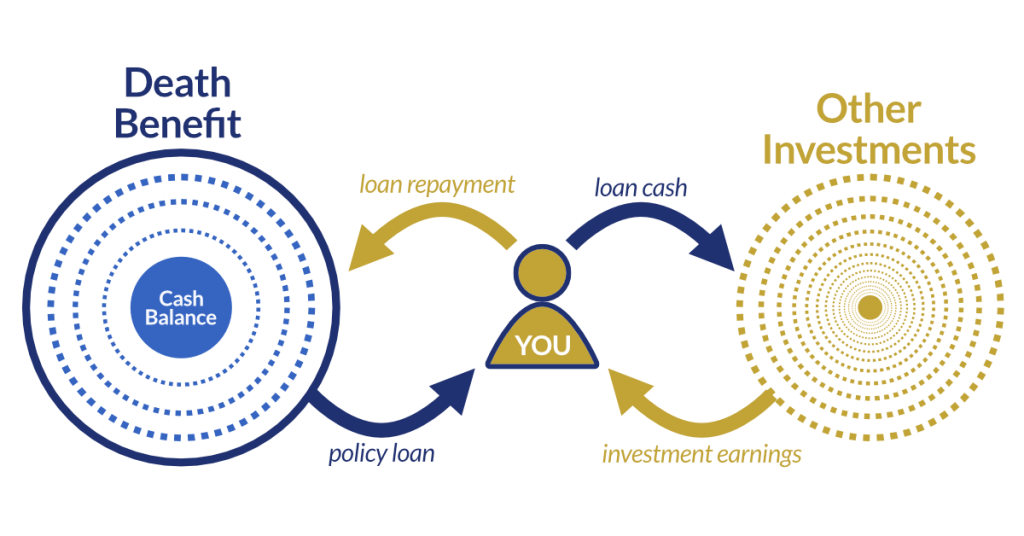

To put it in very simple terms, the infinite banking concept (or IBC) is a method for investing and spending your money at the same time. This is achieved by means of a whole life insurance policy.

Unlike term life, whole life policies feature a cash value or surrender value: the amount you will receive if you decide to “cash out” the policy before you die. This is less than the total death benefit, but it grows closer to that amount over time thanks to 1) your premium payments and 2) the investment of those premiums (part of them, anyway) by the insurance company.

A big perk of this arrangement is that it allows you to easily borrow against your policy – far more easily than borrowing from a bank or even your 401(k). This is because that cash balance acts as built-in collateral. So you can borrow money from the policy at your discretion, while still leaving the cash balance untouched.

And remember, that balance is growing all the while. Depending on numerous complex variables, in fact, it may grow quite a lot. If you then use the policy loan to fund other investments, you effectively end up investing the same money in two places at once.

Powerful stuff… but much easier said than done.

What is the catch?

IBC is often sold as “the secret tool that the rich use to get wealthy.” And yes, wealthy people occasionally have uses for these sorts of insurance policies… but they don’t use them until AFTER they have become rich.

As you may have already guessed, IBC is expensive because whole life insurance is expensive. Part of what makes that cash balance so powerful is the fact that you are funding the policy – early on, anyway – with sky-high premiums. In the projection I ran, those premiums totaled more than $45k a year!

In addition to the huge premium payments, you may notice something else about the above example. Namely, how complicated it is! IBC sounds simple enough in theory; but in practice, getting it to work involves a lot of moving parts that must be carefully calibrated.

And not all those moving parts are in your control. If IBC is to be a practical strategy, your cash balance needs a lot of growth – and that growth depends, at least in part, on stock market returns that may or may not pan out at the right time. That is just one of the many factors to consider.

The bottom line on infinite banking

To sum up, I would say that IBC is a poor strategy for most people. It is definitely not a good way to get rich. But if you have lots of disposable income and big cash flow needs, it may be worth exploring. Just make sure you know that insurance policy inside and out before attempting it.

We like to think that wealth-building techniques only come in two varieties: the proven, reliable, “good” ones (business ownership, a 401(k), real estate) and the hype-driven scams that just rip people off (casinos, crypto trading, multi-level marketing).

But while it is true that some techniques are good for many people, and others are bad for many (very many) people, there is also a big gray area – techniques that can work for some people. Infinite banking falls squarely in that gray area.

Graham Miller uses the trade name/DBA Wiegand Financial Group. All securities and advisory services through Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services are separate from and not offered through Commonwealth.