Important as it is, health care can be a real drag. It is never fun, often unpleasant, and sometimes downright scary. To add insult to injury, out-of-pocket medical expenses can easily become a major roadblock to building up wealth.

A health savings account (HSA) helps by acting as a buffer between your wallet and your medical bills. But few people realize just how powerful it can be as a savings vehicle as well – a real shame in my opinion.

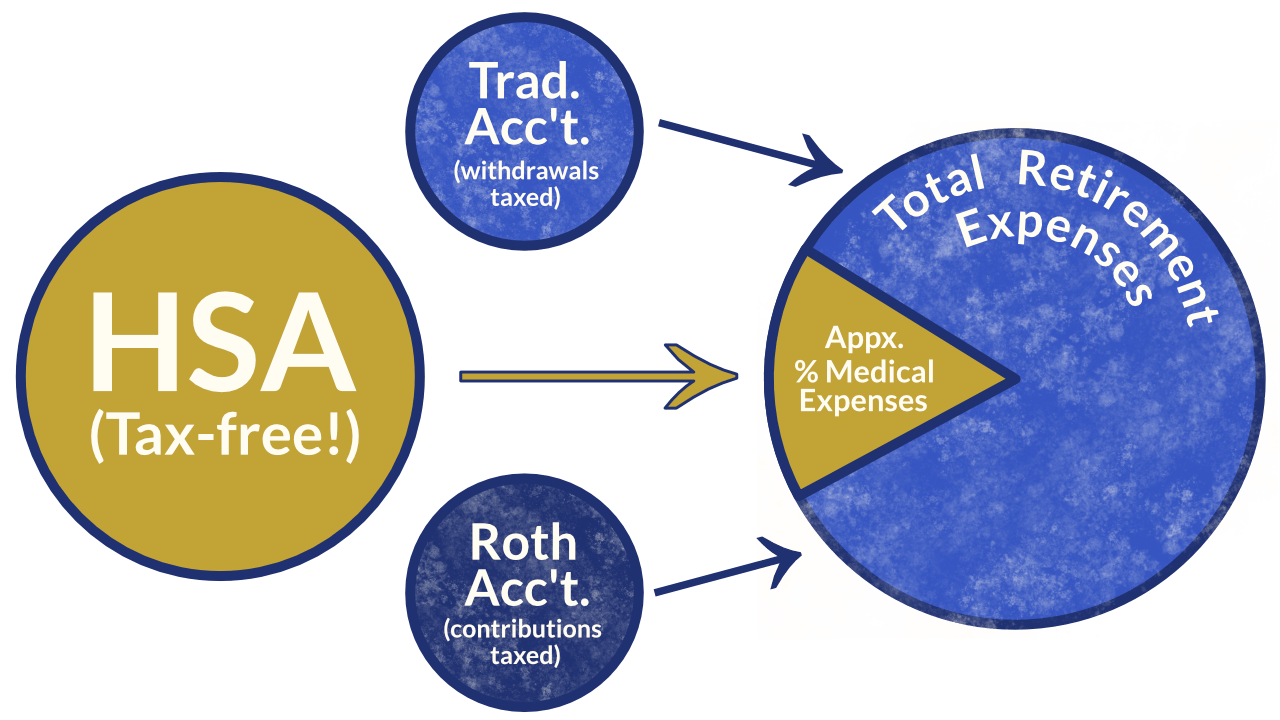

The HSA in a nutshell

Like a 401(k) or IRA, an HSA is a savings account where you place a portion of each paycheck. If you are lucky, your employer may match that amount as well. But unlike retirement funds, which are usually taxed either on the contribution or withdrawal side, HSAs are subject to neither.

To put it simply, HSAs are tax-free savings accounts. That is, your contributions to them are tax-deductible and your withdrawals from them are not subject to income tax (provided you use the funds for eligible medical expenses, anyway). Among other things, this means contributions to the account can pack a real punch if given time to grow!

That “time” is the sticky part, however. While retirement accounts are designed to remain untouched for decades, HSAs often get depleted quickly. They may get cleaned out whenever the next big medical bill comes due, or even be tapped on a regular basis to pay insurance premiums.

There is no requirement that they be used up this way, however. And, in fact, I think it is better to treat your HSA as another retirement savings account instead, provided you have the means to do so.

How to supercharge your HSA

If that sounds like a weird suggestion, consider how most of us can expect healthcare to be a much bigger expense once we are retired than it is now. Not true for everyone, I admit; but if you are in that majority, then saving for health care should be a big part of your retirement prep strategy.

So if you have an HSA, and do not have many out-of-pocket medical expenses, here is how you can supercharge it:

- Make regular contributions to the account;

- Let it grow during your working years by funding medical expenses from other sources as much as possible;

- Use the tax-free proceeds during your Medicare years.

Is investing with an HSA the right move for you?

No deal this good comes without a few strings attached, of course. Fortunately, the IRS is kind enough to update us about them every year, and here are the IRS guidelines for HSAs in 2023:

- FOR INDIVIDUALS:

- Max. HSA contribution = $3,850

- Min. HDHP deductible = $1,500

- Max. HDHP out-of-pocket expenses = $7,500

- FOR FAMILIES:

- Max. HSA contribution = $7,750

- Min. HDHP deductible = $3,000

- Max. HDHP out-of-pocket expenses = $15,000

- NOTE: Individuals over age 55 can make additional “catch-up” contributions up to $1,000.

In case you were wondering, HDHP stands for “high-deductible health plan” – which you are required to have if you want an HSA. And for some, such plans may be more hassle than they are worth. If you do end up with unforeseen expenses before your HSA has had time to grow, an HDHP could leave you on the hook for some pretty big bills.

On the other hand, HDHPs tend to have lower premiums, so that may afford you some regular savings to put toward the HSA. So you are left, yet again, with the question of whether possible rewards in the long term are worth the risk of loss in the short term.

Notice that the out-of-pocket maximum is just about twice as large as the contribution maximum. So at the risk of oversimplifying, look at it this way: if you can get close to the contribution limit this year, and also reasonably expect to cover out-of-pocket expenses for the next two years, you should strongly consider using your HSA to save for retirement. Your future bum knee will thank you.