Two weeks ago we started down a rabbit-hole of retirement prep fundamentals: first by looking at how long-term tax projection can beef up your saving strategy; then, last week, we looked at how to get the most mileage out of your retirement spending through what’s known as a “sequence of withdrawals.”

However, both of these posts – in particular last week’s – left a pretty big elephant in the room: the unpredictability of your stock market investments. This is understandably a major source of anxiety for most (if not all) retirement savers, so we’d be remiss to not dig into it a bit.

The bad news about your rate of return on investment

You may recall that your rate of return (or RoR) is basically the profit you get on your investment over a given period, expressed as a percentage of the total value. Compounding effects can and often do cause those profits to accelerate over time – again, see last week’s post if you’d like a refresher on how that works.

Predicting your RoR is pretty straightforward when it comes to stable assets like CD’s, bonds or even simple savings accounts. But things get much trickier once you’ve got investments that are a little more… chaotic. Like stocks.

2020 was an apt (if a tad melodramatic) illustration of how unpredictable stock market returns can be. At some point any investment vehicle – no matter how bulletproof you think it is – will do something you don’t expect. That theme has emerged repeatedly in the markets over the past eighteen months.

So here’s the big, scary question – how are you supposed to forecast your retirement savings and/or spending over the course of decades, when a big chunk of that money could change dramatically overnight?

Well… to a certain point, unpredictability is inevitable and you’ll have to deal with it. I understand if that fills you with angst; feel free to go scream into a pillow for a couple minutes if need be.

Better? Good.

While I’m not going to lie to you and say that you can eliminate risk in your retirement savings (or any other investment, for that matter), it helps to understand what exactly that risk is. So let’s look at a major challenge your retirement portfolio could face, and one that you may have never heard of: your “sequence of returns risk.”

What you spend and when – why sequence of returns matters

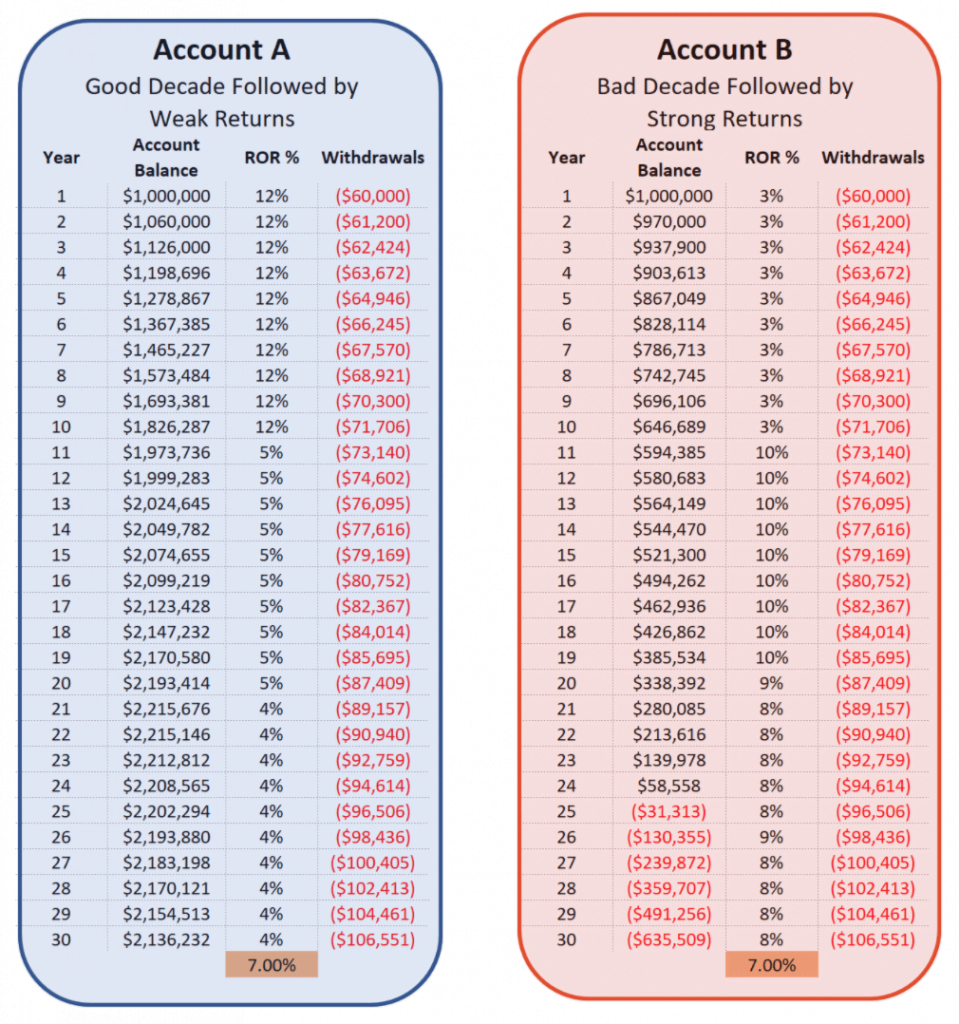

Per usual, it’s helpful to start with a specific example. Say you have two separate investment accounts that both average a 7% RoR over 30 years, have the same starting balance, and that you withdraw the same amount from every year. But suppose that, despite these similarities, “Account A” gets very good returns in the first 10 years while “Account B” only has mediocre returns over that same period.

Spoiler alert: A is going to finish out the 30 years with much more money than B. If you enjoy looking at rows and rows of numbers, take a look for yourself →

But how does that work if they’re identical in terms of starting balance, withdrawal schedule and overall RoR?

Consider compounding returns again. The amount you have at the end of a year is determined by two factors: your investment returns during that year, and the total amount you started the year with. As you gain returns, your total balance increases and amplifies the effects of the next year’s RoR, and so on. If your RoR changes from year to year, the effects of compounding are a lot more… bumpy.

The good news is that this doesn’t really matter if you’re not adding to or subtracting from the account (e.g. during your saving years). If you don’t mess with anything, the ebb and flow of compounding with different RoR’s ultimately cancels out. Doesn’t matter if you have a 5% RoR at first, then a 10% RoR later, or vice-versa.

BUT. That all goes out the window once you start making withdrawals in retirement. Although the average return of both accounts may still be the same over the total 30-year period, the different timing of RoR’s within that period will have a major effect on the final balance.

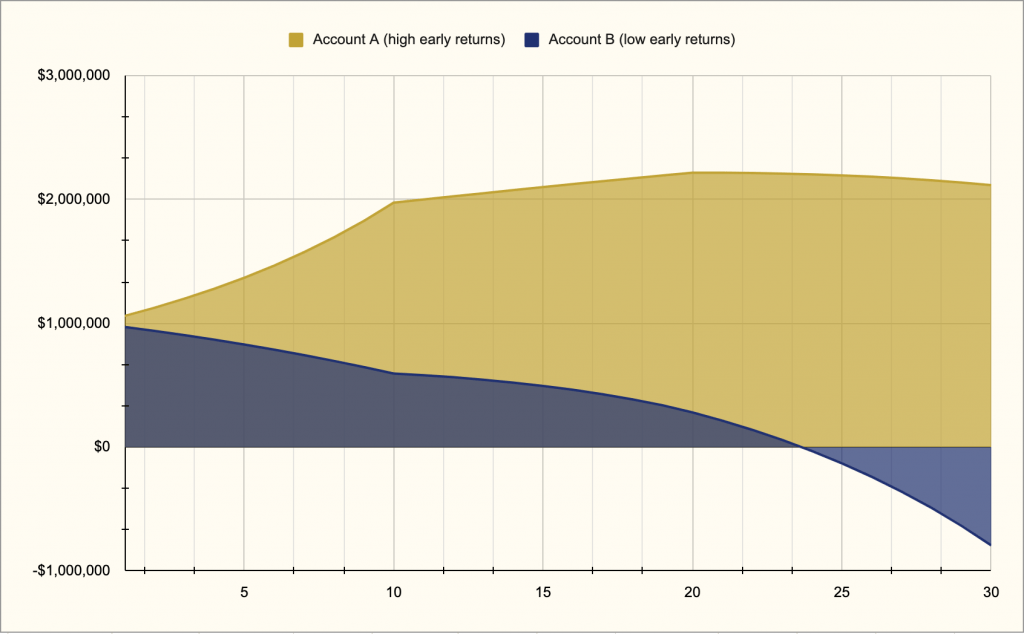

In case that’s all clear as mud, here’s a chart illustrating the respective balances of A and B over 30 years:

Again – same starting balance, same withdrawal schedule, same average rate of return… but Account A has a good first decade followed by low returns, while Account B has a bad first decade followed by 20 good years. This sequence of good investment returns before bad, or vice-versa, is called your sequence of returns.

So even though the RoR in A slows down while the one in B ramps up – the damage has been done. It’s too late for B to catch up, and you have wildly different balances at the end of 30 years.

Sequence of returns risk – and what you can do about it

This possibility, of bad returns early on screwing everything up later, is known as “sequence of returns risk.” And again, there’s no foolproof way to avoid it. Although you can exercise some control over your RoR (namely, by avoiding investments that will make it too unpredictable for what you can stomach), you cannot plan exactly how it will shake out.

In other words, you cannot plan your sequence of returns. But you can make a pretty accurate estimate of how much you will need to withdraw from one year to the next and plan for best-case and worst-case scenarios.

Specifically, you would likely consider investing in both safer investments that will provide you with the cash you will need in the earlier years of retirement AND riskier investments that will provide you with the returns you need to keep your portfolio healthy and able to beat inflation for the later years.

The projections in the above example are just guesses. But they’re educated ones, and therefore serve as guideposts to help you plan around the best- and worst-case scenarios that they illustrate. There’s a lot we could get into about risk mitigation strategies – portfolio rebalancing or just good ol’ cash management, for example – but that’s a whole other post in itself.

Like I said earlier: at the end of the day, you cannot control the market and you cannot avoid risk. But good financial planning, and good retirement planning, isn’t about avoiding risk. Rather, it’s about anticipating it and finding ways to work with it – even to your advantage. And taking a good, hard look at your sequence of returns risk is one of the best techniques for doing so.