As you may have noticed, I like picking apart investment rules of thumb. And it is once again time for the annual classic: “sell in May and go away.”

I hear this old proverb every single year around this time, ad nauseam. But where did it come from? What does it mean? And is it a reliable rule?

Why “Sell In May and Go Away”?

This rule assumes that markets slump in the summertime, as people leave off trading activity in favor of their RVs, fishing cabins or beachside rentals. If overall market activity goes down – the thinking goes – then your returns will too. So you may as well sell off your riskier assets and put your portfolio on autopilot until November.

This reasoning makes sense to an extent. But it likely made way more sense to the wealthy merchants and financiers of 19th-century England where it supposedly originated. For them, “summer vacation” often meant staying at a countryside manor for months, removed from urban business centers by a lengthy train or carriage ride.

In an age where most – if not all – financial transactions required either your physical presence or a weeks-long mail exchange, this would put a legitimate damper on market activity. Now, however, Wi-Fi and mobile apps allow investors to keep up with the markets anytime, anywhere. Yet the “sell in May” strategy still has wide appeal.

Does it still work?

One major reason for the rule’s success is that it is self-reinforcing. If enough people exit the market because they do not expect much action over the summer, sure enough: there will not be much action over the summer. As a result, more people will do the same the following year, and the one after that, and so on. Who cares if you have 5G?

But the circular logic of crowds is just one of many, many, many factors that impact market returns. And recent history suggests that a fair bit still happens in the markets during those summer months – and that those snowbird investors are missing out.

Selling in May today

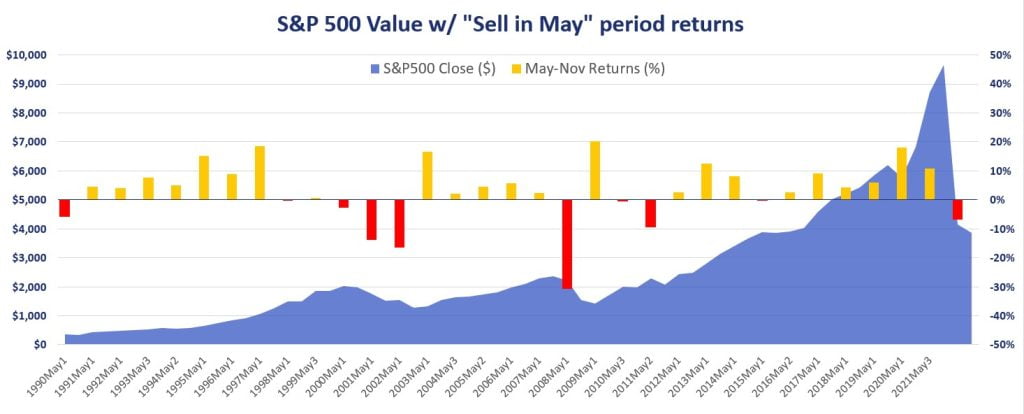

If we look at overall market performance since 1990, we find that there have been only ten years where the “sell-in-May” strategy would have paid off (one of which, unsurprisingly, was last year). Across those ten years (highlighted in red below), the May-November “off-season” averaged a -8.66% return:

So yes, you might have dodged a bullet by sitting out those summers. But across the other twenty-three years, off-season returns averaged +8.25%. In other words, you would have given up twenty-three years of good returns in order to avoid ten years of bad ones. Not a good trade-off.

And if we chart out that performance in contrast to that of the overall market, it looks like a downright bad trade-off. If you invested $10,000 in the S&P 500 in 1990, here is what would have happened to it with and without those summertime selloffs:

I will admit that 2022 gave us a good demonstration of the rule’s appeal – as you can see, selling in May softened the blow considerably for our hypothetical portfolio last year. But in the long term, the strategy still leaves that portfolio $93k short of where it would otherwise be!

Now, perhaps some would consider that extra $93k to be an acceptable loss, in exchange for the privilege of sitting poolside and sipping watered-down mojitos for weeks on end without a care in the world. Again, there is no absolute right or wrong answer here – it depends on your personal priorities.

But personally, I think leaving that much dough on the table would be a real bummer. In any case, the sell-in-May strategy is clearly no longer useful enough to be called a rule. A good replacement might be, “if your investment strategy rhymes, then it probably doesn’t work.”