It may be spring outside and Easter on the calendar, but that doesn’t necessarily make the financial atmosphere warm and sunny. If anything, it seems like a new boogeyman has joined the others already creeping around the headlines – a little something known as stagflation.

If you’re not familiar with the term, it may sound rather nonsensical. And that wouldn’t be entirely wrong, as it’s not the most technical term and rather poorly defined. But I’ve heard it tossed around a lot lately, with many gloom-and-doom comparisons to the 1970s oil crisis that are sure to be alarming.

So let’s consider: what is stagflation, and is it a real threat at the moment?

What is stagflation?

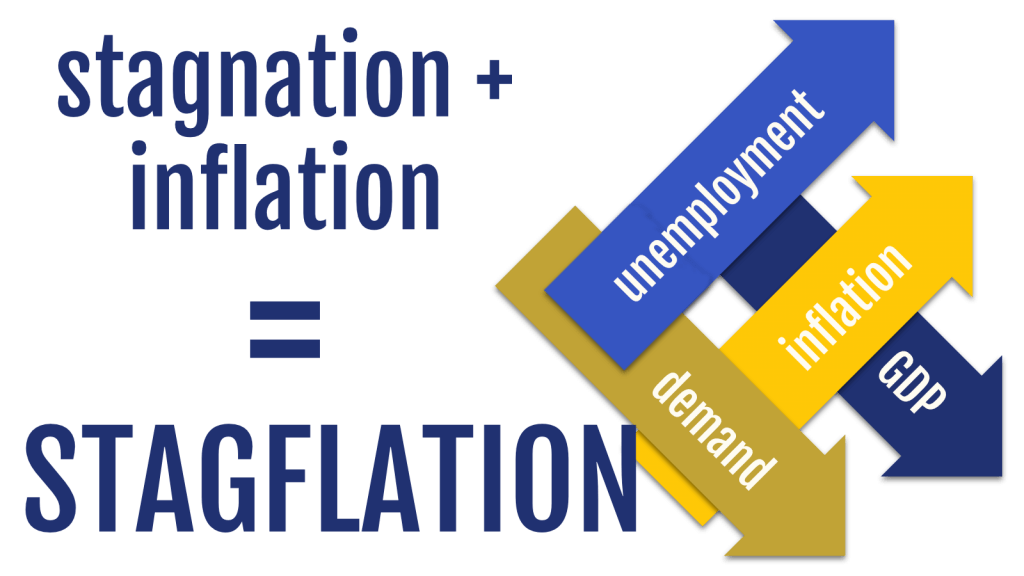

A mashup of “stagnation” and “inflation,” stagflation basically refers to inflation during a period of recession. And when the two coincide it’s the worst of both worlds.

A recession is generally understood as two or more consecutive quarters of negative GDP. When economic activity slumps like this, unemployment rises proportionally – always bad news. But during normal recessions prices tend to fall, which is at least a small comfort to consumers.

Not so with stagflation, however, where prices stay elevated despite a scarcity of jobs and declining production.

This was the case in the UK in 1965, where politician Iain Macleod first coined the term in a speech to Parliament. And it quickly became relevant in the States as well, as unemployment and inflation both peaked in the mid-70s.

When has it happened before?

As in any other science, we can only make economic predictions based on data about what has happened in the past. So, what has stagflation looked like previously, and how do those situations compare to today?

We know that stagflation happens when high inflation meets recession meets high unemployment. Let’s start with the variable that we can define most precisely: recession.

Per the criterion mentioned above (2 or more quarters of negative GDP), we can identify 11 recessions in the US since the 1950s, as shown by the grey bands here:

Now the question is: which of these 11 periods also had high inflation and high unemployment?

But that immediately poses another question: how high is “high?” There isn’t much consensus on that point, which makes it hard to identify what counts as stagflation and thereby gather historical data on it.

For the sake of argument, let’s say that we’re looking for inflation and unemployment rates that are at least 10% above average during a period of recession. No need to squint at the chart; I’ve already done the number-crunching and found some contenders:

What does this tell us? Well, um… not much we didn’t already know. That first period is the archetypal mid-70s one, and the last one – the 2008 recession – barely qualifies at all, to be honest. Which leaves those two back-to-back periods in the early ‘80s.

But those have their own complications. Note that inflation, while elevated, fell precipitously over those periods while unemployment climbed. So while the numbers might fit our ad-hoc criteria, the overall trend looks consistent with normal recessions.

We could of course find out more by really digging into the economic details of the time, like the geopolitical landscape or what monetary policy looked like. But that would almost certainly raise even more questions – and we’re trying to eliminate ambiguity, not add more of it. Our data-gathering experiment is a bit of a bust.

Are we headed for stagflation?

The core concept of stagflation is fairly straightforward – and frightening to boot – which makes it great for headlines. But much like “recession,” the term is best used historically rather than predictively, to describe an economic landscape like that of the mid-70s after the fact.

Unlike “recession,” however, the term lacks technical clarity in its definition. And this makes it kind of useless for rigorous market analysis, whether historical or predictive.

Thanks to that ambiguity, there are various ways to convincingly “predict” stagflation:

- One could potentially argue that we should expect a recession.

- One could also argue that we should expect higher unemployment.

- And one could certainly argue that we will experience sustained inflation.

But in order to make a really slam-dunk case, you need to clearly demonstrate all three of those things – and I just don’t see anyone pulling that off right now.

To see what I mean, let’s zoom in on the last decade of that chart:

Yes, we are experiencing impressive inflation; but current data does not indicate recession and unemployment rates are extremely low. So as the numbers stand right now, the ingredients for stagflation are simply not yet present.