Most of us assume that there’s a certain lump sum we’re just going to have to pay in taxes every year. Our CPA looks over a bunch of forms, plugs some things into a calculator, gives us a number and that’s it.

Sure, maybe there are some credits or deductions that we overlook from time to time, but the whole thing is so complicated that it’s just easier to pay that lump sum every year and move on.

That’s one approach, and I get it. But the thing is, you probably have more control than you realize over how much you owe in taxes (also known as your “tax liability”). This is especially true if we’re talking in the long-term. Your options are pretty limited when it comes to this or even next year’s taxes. But the choices you make today can have a huge impact on your total tax liability over the course of decades.

A different approach to tax projection

You may be familiar with the term “tax projection,” especially if you’re a business owner. Even if you haven’t heard that term before, you’ve probably done it: it simply means looking ahead to anticipated future income, tax bracket, life changes and other factors, and accordingly coming up with an estimate for your future tax liability.

But I want you to think about an application of this concept that many people don’t consider. When people do a tax projection or even just talk about it, it’s usually in terms of the next year or so. I’m more interested in tax projection over the long term, however.

Don’t get me wrong – short-term tax projection makes sense, especially when you’re younger. All sorts of things could happen within the next few years to completely upend your tax status: a new job, a new baby, inheriting your uncle’s home-distillery business, whatever.

But people often underestimate the number of long-term factors they can reasonably plan for, and don’t consider how such factors may affect their financial situation decades down the road.

For example, if you’re currently making contributions into an IRA or 401(k), you can expect to start withdrawing from that account once you’re 59½ years of age – as the law stands now, that’s just a fact. Even if you’re still 25 years away from that point, you can still plan on it. Tax law doesn’t exactly change quickly, which means that you can pretty accurately predict how much tax liability you’ll have in your savings and investments, even decades down the line.

In short, while long-term tax projection doesn’t get a whole lot of publicity, it’s a powerful tool and one worth exploring.

Saving strategy looks different for everyone

To illustrate this, let’s consider the example of a young professional who –

- Is 30 years old currently

- Wants to retire at age 60

- Intends to put away $2,000 in savings every month until then.*

- *Not sure how many 30-year-olds are in that kind of position nowadays, but 2,000 is a nice round number, so let’s go with it for now.

And let’s say she’s considering three possibilities for where to invest this money. All three accounts promise an 8% rate of return, compounded annually. However, they are each taxed very differently. Her three choices basically break down as follows:

- Regular old brokerage account – Fully taxable, meaning that the growth of your investments is subject to tax, and contributions to the account aren’t tax-deductible.

- Traditional IRA – Tax-deferred, meaning that contributions to the account are tax-deductible, but withdrawals are also considered taxable income.

- Roth IRA – Withdrawals are tax-free, but contributions aren’t tax-deductible.

All three of these accounts present an advantage to our hypothetical investor, in that they’ll grow her contributions considerably over the 30-year period she plans to invest.

But the total return from each will be very different, and the size of that difference depends on a couple of other variables. Key among these variables is the tax bracket she’s in: how high it is, whether it’ll change, and whether she cares if it changes. So much of financial planning depends on what your priorities are, and this is a perfect example. For some people, greater income is worth potentially jumping to a higher tax bracket; for others it’s not.

Let’s say our example investor wants to maximize her monthly retirement payment, but without jumping into a higher tax bracket by doing so. In fact, let’s say she expects to be in a slightly lower bracket: without kids or a commute to worry about once she’s retired, she can simplify a bit.

With this in mind, here’s the big question: once she’s retired, which account type (brokerage, IRA, or Roth) will allow her to withdraw the biggest monthly amount, after taxes?

Taxable, Tax-Deferred and Tax-Free accounts over time

Let’s assume that Li’l Miss Hypothetical will be in the 24% tax bracket during her working years (i.e., when she’s saving up); then, when she hits retirement (i.e., starts withdrawing), she’ll drop into the 22% bracket.

When we plug everything into our handy algorithm, this is what we get:

Each curve represents the total balance over time of one of those three accounts. The peak, as you can probably guess, is the point where she stops contributing to the account and starts withdrawing instead.

Notice how wide the gaps are between each curve, especially when you consider the amounts of money at play here. It pays to save, kids!

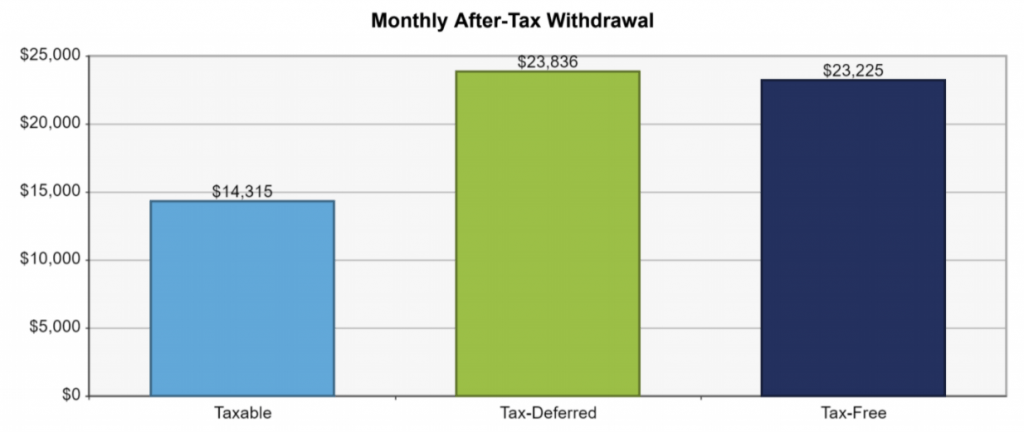

But as sleek and clean as this chart is, it doesn’t quite give us the info we’re looking for. Again, it shows the total yearly balance over time, and we’re more interested in which account will give her the biggest monthly payment, after any applicable taxes.

Fortunately, our faithful algorithm can also show us what that looks like:

Looking at both charts, the conclusion is clear: the tax-deferred account gives the best return in this particular situation, both in terms of overall account balance and in terms of monthly payout. A slim lead, yes – but one that really adds up over months and years!

Maximize your retirement income by doing the math!

It doesn’t take much explanation to see why this result is surprising. Most of us would probably expect the biggest return from the fully tax-free account. But that’s not how it actually turns out here.

How ‘bout that! And our starry-eyed young investor wouldn’t have ever seen it coming if we hadn’t crunched the numbers for her.

I could go into the reasons for why the tax-deferred account performs better, but I want you to actually read to the end of this post, so I won’t. The point is to illustrate how big an effect taxes can have over the long term.

Yes, we all want to minimize our taxes this year, or the next… but thinking with a wider view can be much more beneficial. Less tax in the short term isn’t always better in the long term.

Of course, it’s easy to see the big effect that taxes can have over an investment period of 30 years. But what about a spending period that, conceivably, could be just as long?

Well, that’s why this is another two-part post.

Saving for retirement can be hugely affected by taxes over time, and therefore benefit from smart strategy – but the same is true once you start using those savings as well. So next week, we’ll take a look at how to apply tax strategy to your retirement income: that is, how to spend your money as efficiently as you save it.