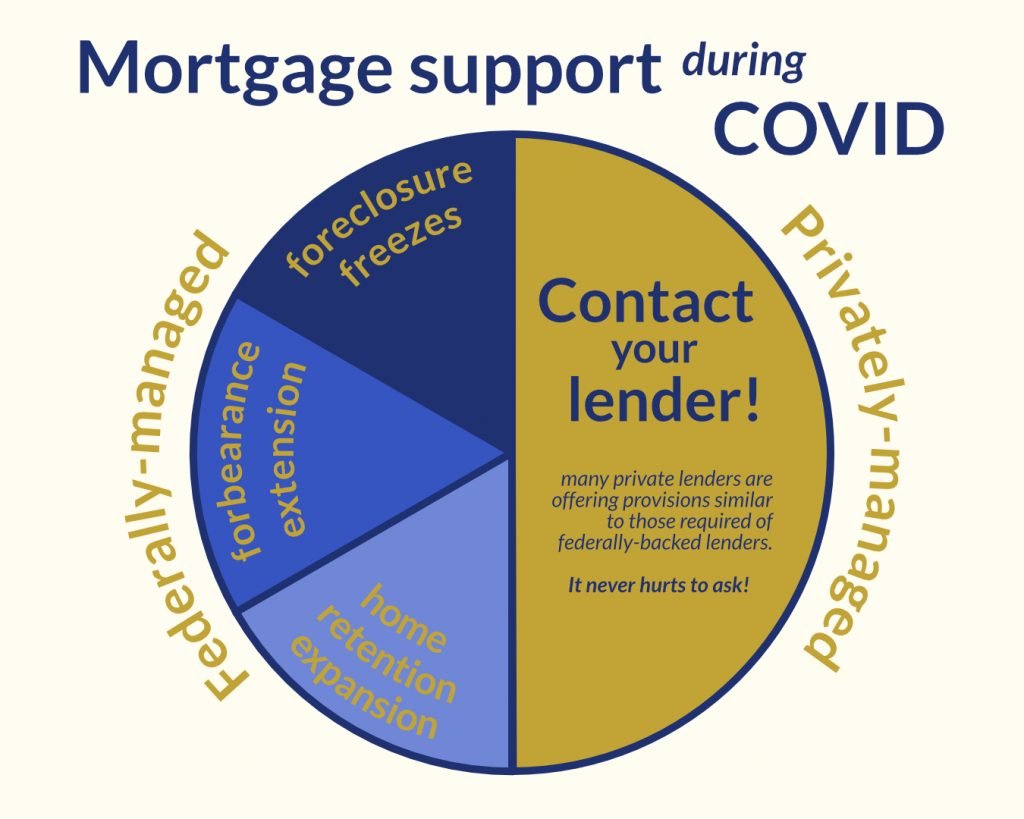

For homeowners, mortgage payments can be a real pain amid the financial chaos of COVID – but the good news is that temporary relief may be available. Thanks to the Coronavirus Aid, Relief, and Economic Security (CARES) Act passed in March 2020, you may be able to delay your payments on federally owned or backed mortgage loans by placing those loans in forbearance.

A mortgage placed in forbearance will keep accruing interest, as it isn’t forgiven or removed. But you won’t have to continue your regular payments on it during the forbearance period – 180 days in this case. You may qualify for forbearance if:

- You’ve experienced a COVID-19 hardship such as loss of a job, reduction of income, or sickness; and

- Your mortgage is federally owned or backed; i.e. if it comes from an entity such as –

- The U.S. Department of Housing and Urban Development

- The Federal Housing Administration

- The U.S. Department of Veterans Affairs

- The U.S. Department of Agriculture

- Fannie Mae

- Freddie Mac.

And if you aren’t sure whether your mortgage is eligible, the Consumer Financial Protection Bureau has tools to help you look up which organization owns your mortgage.

Even if you don’t have a federally backed mortgage, you may still have options. Some states have provided temporary relief from certain foreclosures or evictions, and many companies are also providing a range of mortgage relief options. So no matter where your mortgage comes from, if COVID has made it hard for you to keep up with it, it’s definitely worthwhile to get in touch with your loan servicer.