If there’s one thing that Americans left and right alike seem to agree on, it’s that China is our biggest geopolitical boogeyman. Up to this point – halfway through his term – Biden hasn’t touched the sweeping tariff package on China that was one of Trump’s dearest darlings. That’s saying something.

But word on the street now is that’s all about to change. In the name of fighting an even bigger boogeyman (inflation, again), the Biden administration has announced that it will soon roll back those Trump-era tariffs.

Or some of them, anyway. Maybe. But also maybe not. It depends.

Investors, of course, hate wishy-washy news like this. The taxation of imports between the world’s two biggest economies has huge implications for prices across the board, so it would be really nice to know ahead of time if something is going to change there! But we don’t know – so what do we do??

The trouble with tariffs

As a tool in global trade competition, tariffs are notoriously double-edged. A nation may use them to give a competitive edge to domestic producers of a given commodity. By taxing the heck out of that commodity when it’s imported, they make the foreign version more expensive and the domestic one more appealing by comparison. In theory.

But at the risk of stating the obvious, remember that the nation’s citizens are the ones paying that tax. So if domestic producers don’t make enough of Commodity X to keep up with demand, it will just get more expensive across the board… and their foreign competitors will still dominate the market. According to many commentators, that is exactly what has happened with Trump’s tariffs.

I don’t know if that’s objectively true, but it’s easy to see why people think so. In 2020, for example, China was still unmistakably ahead of domestic producers in two of three top sales categories:

Regardless, rolling back these particular tariffs presents a major political hazard. Plenty of Americans want to keep manufacturing alive and well in this country – labor unions being a chief example. For many of those, keeping the tariffs is a no-brainer. In fact, as our huge trade deficit with China has only gotten bigger since the pandemic, it seems downright urgent.

Splitting the difference

That all gives you context for the following point: any tariff rollbacks that Biden implements will likely have a negligible effect. Caught between fighting inflation and staying tough with China, Biden’s administration is looking to either split the difference or do nothing at all. If implemented, the proposed changes to Trump’s tariffs would apply to just about 3% of Chinese imports.

Leaving aside the fact that 3% is a tiny fraction of the Chinese goods in American markets, even a total reversal of Trump’s policy likely wouldn’t make much difference to our current problems. As we’ve discussed elsewhere, today’s inflation is due largely to supply chain issues and energy scarcity – neither of which would be affected by making Chinese imports more affordable.

Another approach

So… why take all this time to explain something that’s not actually a big deal? In part, to remind you that the topics that get a lot of press (and/or throw investors into a tizzy) aren’t always that significant under the surface. And sometimes they even obscure other topics that are perhaps more important.

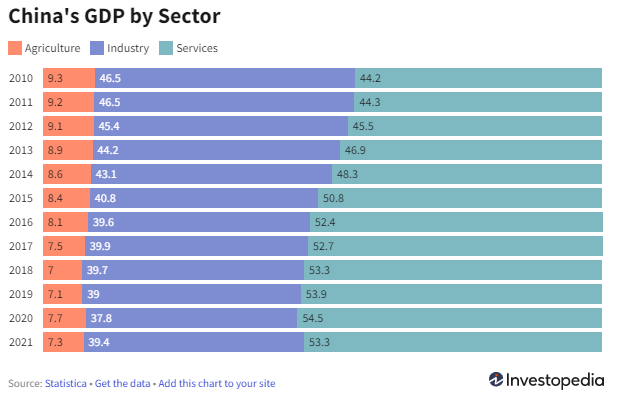

For example, with all the talk about our trade deficit with Chinese manufacturing, it’s very easy to overlook something like, say… the growing prevalence of China’s service sector.

Although we’re very accustomed to seeing that “Made in China” stamp on the bottom of everything, could it be that China is making the shift from a manufacturing/ export-based economy to one more service-based like the US? If so, the next manufacturing hot spot may be worth investing in… but you may need to look beyond the headlines to find it.