I recently had a doozy of a question put to me (not by a client): “I just turned 59½, my net worth is $3 million, and I have $240k in credit card debt. Should I use my IRA, annuity, etc. to pay down that debt?”

My first reaction was “wait, what? Did you say $240,000 in credit card debt?”

Unfortunately, the question was posed secondhand and I therefore could not ask the asker how they managed such a feat. It is still a mystery to me. But despite the craziness of this situation, the question at the core of it is straightforward enough: should you pay off debt with your IRA or other retirement savings?

In most cases, my answer would be “no.” But perhaps this case is an exception. If you are up to your eyeballs in high-interest debt, is that a good time to tap your retirement savings?

An example: paying your credit card bill from your IRA

First, let’s make this example just a bit more relatable and bring that credit card balance down to $50k. Let’s also assume the following of our questioner:

- Makes $100k in taxable income;

- Current IRA balance is $1 million;

- Credit card charges 19% interest.

With those in mind, we want to determine which of the following options for paying off that $50k will be less costly in the long run:

- A one-time withdrawal from the IRA; or

- Monthly payments from income over 3 years.

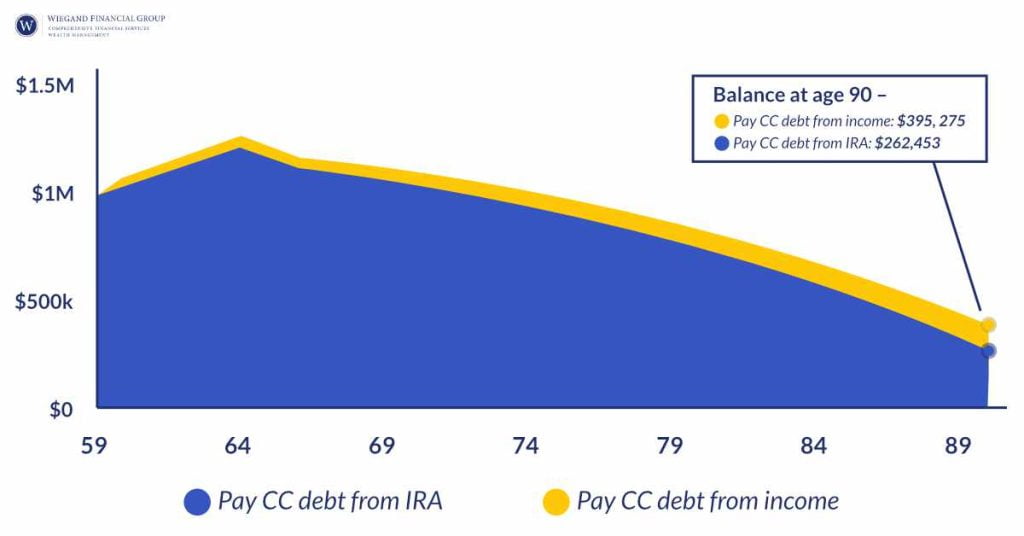

One way we can do this is to run a projection on the IRA balance with and without that $50k chunk withdrawn. The green segment below shows the difference:

It may not look like much compared to the overall savings – but compared to the debt itself, the difference is huge.

Is it worth it?

One big problem with using retirement savings in this case is that a $50k withdrawal will generate an extra $10k of taxes. If the withdrawal is made prior to full retirement age, the problem is worse – penalties kick in and the extra tax is more like $16k.

Another problem (as we saw just a couple weeks ago) is that big withdrawals from your portfolio have big consequences over time. Supposing our questioner lives to a ripe old age of 90, their portfolio will have missed out on over $130k when all is said and done.

As bad as that sounds, however, it is worth noting that the portfolio still stays in the black – so perhaps this scenario is better than the alternative. For many, having a pile of present-day debt is more serious than being hypothetically less-rich in the future. Especially if that debt charges 19% interest.

So perhaps getting rid of that debt now is worth the price tag later. The key, of course, is to know the price tag ahead of time.