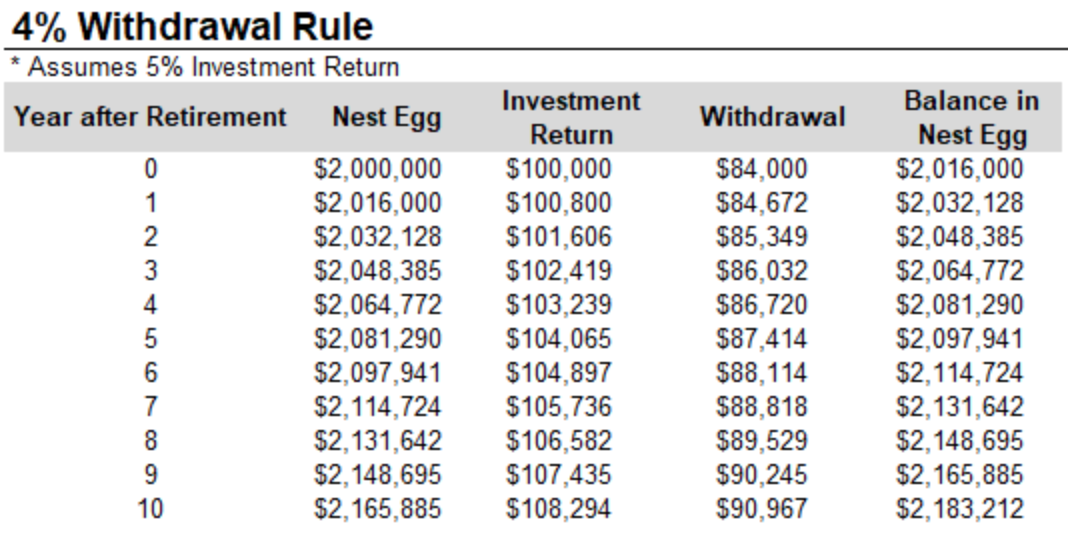

The “4% Rule.” I know you have heard of it! This far too widely used rule of thumb suggests that an initial withdrawal rate of up to 4% of your nest egg (increased for inflation each year) will allow the portfolio to sustain the withdrawals for any 30 year retirement.

But why 4 percent? Why not 3%, or 5%, or 4.726%?

The rule comes from Bill Bengen, an advisor in California, who published some research in the early ’90s which suggested that a portfolio with the classic 60/40 mix of stocks and bonds, would survive worst-case market scenarios if their withdrawal rate was 4.15% or lower.

He came to that figure by testing various withdrawal rates against actual stock & bond market performance from 1926-1976. Withdrawing even 5% would cause his hypothetical account to eventually hit zero. In other words, he found that 4.15% was the most that retirees could safely withdraw – during that particular 40-year period, anyway.

Bengen’s findings got passed around a lot, but unfortunately – as often happens when things “go viral” like this – people cherry-picked his data for handy slogans, rather than keeping the whole context in mind. Soon his 4.15% figure had been rounded down to 4%, and it was being treated as a timeless law for all retirees.

It’s ironic to the point of being funny. Bengen’s “creation” of the “rule” was not only accidental, but in fact counter-productive: the whole reason he did that research in the first place was to cross-examine other rules of thumb that were popular at the time.

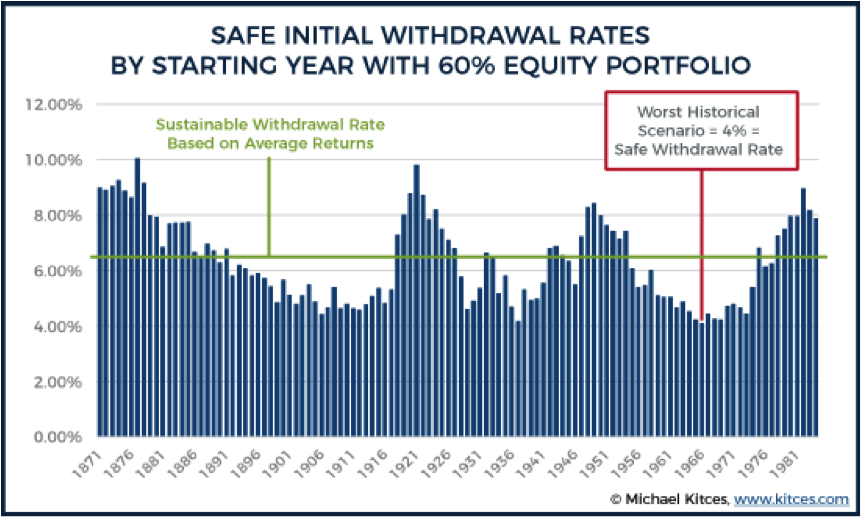

In short, this is a nice ‘back-of-the-napkin’ guideline… but never in a million years would I base my financial future on it. It is predicated on factors that vary a lot from one individual to the next and, most importantly, relies on historical data. Take, for another example, the average withdrawal rate from a hundred-year span of data:

In the end, there is no one rule that will guarantee the longevity of your nest egg. While the 4% rule may serve as a rough starting point, your portfolio will not receive the same sequence of returns that a 60/40 portfolio experienced in the 1970’s.

In other words, nothing can really replace a financial plan tailored to your unique needs – and skepticism is usually wise with these “one size fits all” maxims.