As with all professional services, financial advisors may have biases or conflicts of interest. Ironically, advisors can get a lot of marketing mileage from appearing to eliminate conflict of interest in their practice, regardless of whether they actually do so.

A great example of this is the “fee-only” fad currently sweeping the financial advisory world. There are many different business models for financial advisors, but one big distinction is whether they are fee-only or fee-based. In brief:

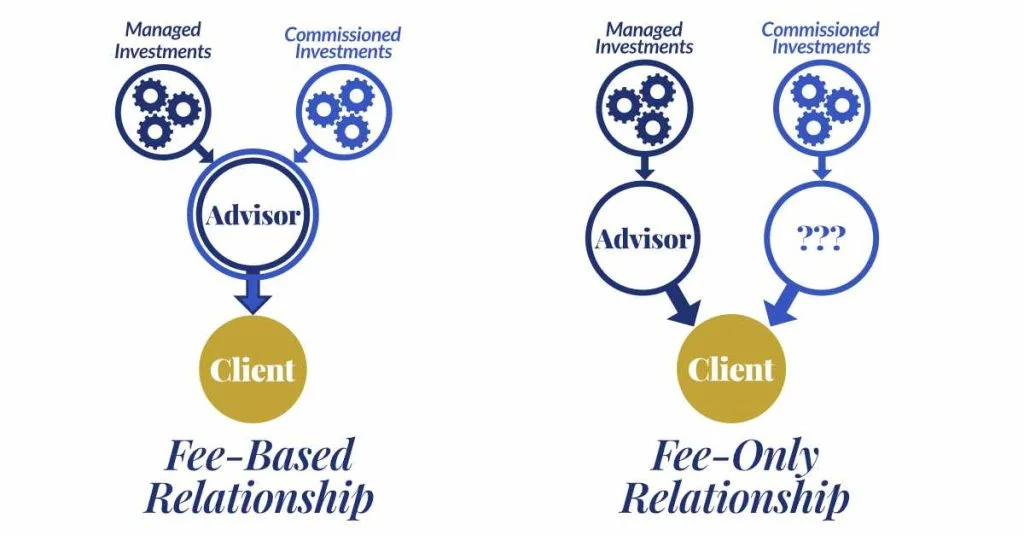

- Fee-based: Charges a fee for service, may also receive commissions if they use certain third-party investments (annuities, REITs, etc.).

- Fee-only: Charges a fee for service, may not ever receive commissions nor use investments that pay them.

The common claim is that fee-based advisors are vulnerable to conflicts of interest, while fee-only advisors are not. But this is a huge oversimplification for multiple reasons.

The many flavors of conflict of interest

Many advisors – fee-only and fee-based alike – charge their clients a percentage of AUM (assets under management). If your advisor charges you an AUM fee, and they determine some of your money would be better utilized with a third party, this presents a classic conflict of interest. Any money of yours that leaves their management means they earn a lower fee.

However, although the fee-based advisor will earn less from you in this case, he may still be compensated by that third party. This mitigates the conflict of interest for him. The fee-only advisor, on the other hand, has a one-sided incentive to keep all your investments in-house, and thus faces a stronger conflict of interest.

There are also advisors who charge their clients a flat fee or an hourly fee. Such advisors do not lose anything by referring you to third-party investments. But if they are fee-only, they must refer you to that third party rather than brokering the transaction themselves. In that case, you end up paying your advisor’s flat fee and the commission. With a fee-based advisor, you only pay one or the other.

The fiduciary difference

“But Graham,” you may ask, “if a commissioned product ever were appropriate for me, wouldn’t a fee-only advisor have a fiduciary duty to send me elsewhere to get it?”

Absolutely. But by the same token, the fee-based advisor also has a fiduciary duty not to schmooze you. In short, neither fee structure guarantees the advisor will act in your best interest. Conflicts of interest can and do take many different forms, which is why the fiduciary designation exists in the first place.

None of this is to say that the fee-only model is bad, by the way. It has its benefits and its drawbacks like anything else, and will be a great fit for some. But hyping it up as objectively superior does not work to investors’ advantage. I have an example to illustrate how this works.

The cost of hype

Although annuities are normally commissioned products, annuity companies are starting to offer versions of them where the advisor can “attach” his normal fee rather than charging a commission. I can only assume this is because they are – understandably – trying to cash in on the fad.

I rarely use annuities, but last year I was shopping some for a client and noticed something odd. Although the annuities on offer were nearly identical, the “commissioned” one would have paid my client $24,517/yr for life. The “fee-only” annuity, on the other hand, would have only paid about $21k/yr.

Had I been a fee-only advisor, I would have been able to get my client an ostensibly “guilt-free” annuity… but he would have missed out on $3,500/yr for the rest of his life! Fortunately, I had access to the market that product was designed for, and was thus able to get it for my client at a good price.

And that is because I am still a greedy, conniving, fee-based advisor.